The investing information provided on this page is for educational purposes only. NerdWallet does not offer advisory or brokerage services, nor does it recommend or advise investors to buy or sell particular stocks, securities or other investments.

Welcome to NerdWallet’s Smart Money podcast, where we answer your real-world money questions.

In this week’s episode, we’re sharing NerdWallet’s recent webinar, which was about inflation.

Check out this episode on any of these platforms:

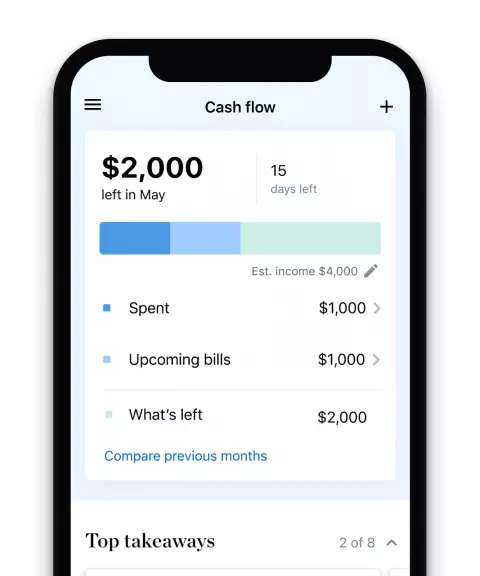

Before you build a budget

NerdWallet breaks down your spending and shows you ways to save.

Our take on inflation

During NerdWallet’s inaugural NerdTalk webinar, a panel of Nerds explained how inflation works, its impact on household finances and strategies for protecting and growing your money.

Inflation affects the prices of goods and services, which decreases our purchasing power. The current inflationary period has been especially severe as essentials like food and gas have increased at their highest rates since the early 1980s. The Federal Reserve is fighting inflation with periodic rate hikes to make borrowing money more expensive in the hope of slowing consumer spending. While we wait for inflation to subside, follow some of the Nerds’ tips for maximizing the value of your dollar.

If you’re looking to spend less, you could cut unnecessary expenses from your budget or switch to cheaper products or services such as a different cell phone provider. Apps like Flipp and GasBuddy can help you find the lowest prices on food and gas, respectively.

As credit card interest rates rise in response to the Fed’s rate hikes, you may feel a sense of urgency to pay off credit card debt. To do so, choose a debt payoff strategy that suits your financial situation and personal preferences. Consider a 0% annual percentage rate balance transfer credit card if you want to consolidate balances from multiple credit cards and get a reprieve from interest.

You can also combat inflation by increasing your income. You might negotiate a raise, move to a higher-paying job, take on a side hustle or park your savings in a high-yield savings account.

If these strategies are not enough to keep you financially secure, access resources like 211.org for food, housing and health assistance or the National Foundation for Credit Counseling for help managing debt.

More about inflation on NerdWallet:

Episode transcript

Sean Pyles: Inflation is doing more than making my beloved cream cheese more expensive at the grocery store. It’s changing virtually every aspect of our finances. Welcome to the NerdWallet Smart Money podcast. I’m your host, Sean Pyles.

A few weeks back, Smart Money host Liz Weston led a webinar with a handful of Nerds where they went deep into what inflation means for your money. And it was so good that we wanted to share it with our podcast listeners.

So give it a listen and let us know if you have any questions about how to navigate inflation, including how to use it to your advantage. Leave a voicemail or text the Nerd hotline at 901-730-6373. That’s 901-730-NERD. Or email [email protected] All right, here’s the webinar.

Liz Weston: Welcome, everyone, and thank you so much for joining our first-ever NerdTalk webinar. We’ve gathered some of our expert Nerds today to talk about inflation, break down what it really means, how it affects different aspects of your financial picture and goals, plus what you can do to protect and grow your money.

With me today to help answer your questions about inflation are data journalist Liz Renter, personal finance columnist Kim Palmer, credit cards writer Melissa Lambarena, personal finance writer Chanelle Bessette and mortgage reporter Holden Lewis. I’m Liz Weston. I’m a personal finance columnist for NerdWallet.

We’ll have time for a few questions at the end, so please feel free to ask questions anytime as we go along using that Q and A button at the bottom of your screen. We’ll try to answer as many as we can today, and we’ll also send some more resources after the webinar that may help you answer your questions.

Also, quick legal disclaimer, we are not financial or investment advisors. This nerdy info is provided for general educational and entertainment purposes and may not apply to your specific circumstances.

So we’d like to start by hearing from you and how you have felt inflation personally. So there should be a poll popping up pretty soon, and you can click on the answers that apply to your situation. It’s multiple choice. Whether you felt inflation in food, clothing, gas, housing, utilities, and there’s also an option if you haven’t felt it that much.

OK, so the results. Food, 80% of you said you felt it in food. Gas is another big one. Housing, oh, man, the rent increases lately have been crazy. Utilities, natural gas prices off the charts. And 6% of you said you haven’t felt it much. OK, well good. I’m glad you’re here anyway.

So let’s talk about what inflation actually is because you’re not alone if you’re a little fuzzy on the concept. NerdWallet recently did a survey that found that 3 out of 5 Americans who were polled are confused about what inflation actually is. So, Liz Renter, what do you say?

Liz Renter: Hey, everybody. So, yeah, you’re not alone. I mean it’s hard enough to answer that in a multiple-choice question, but if somebody just came up to you and said, “Define inflation,” I think a lot of people would be struggling for words, but it’s a pretty easy concept.

It’s rising prices. It’s the rate at which prices are increasing, and that means prices across all goods and services, all the things on that quiz that you just took and then some, right? It’s generally presented as a 12-month percent change. So when you hear inflation is at 7%, what that really means is inflation, or prices, have grown 7% in the past year.

So as a result of inflation, as a result of prices rising, the purchasing power or the value of your money decreases. A $5 bill in your hand buys less and less as prices go up and up. So that’s how you feel it.

And inflation is just part of the economy. It comes, and it goes. It’s a hot-button topic right now because it’s risen to levels we haven’t seen in 40 years. So I guess bottom line, to answer your question as simply as possible, inflation is high, it just means that prices are high and getting higher.

Liz Weston: OK. So why is inflation happening like this now?

Liz Renter: Well, so in general, and if there are any — I don’t think you’d come to this call if you knew all the ins and outs of economic theory and inflation — so I’m going to simplify things a lot here because it is a big topic and it’s very, very complex. But I think in general we can say that inflation comes from either supply or demand, and right now we’re experiencing some of both.

So the supply-side inflation is caused by economic shocks, so things like war or a global pandemic. We’ve seen several of these shocks over the past few years, and throughout history you’ll often see it tied to periods of high inflation. So inflation caused by those supply-side shocks is largely considered transitory or temporary, and the further we get from those shocks, the more they dissipate and inflation comes down. But they do cause friction in the supply chain. The goods and services have a hard time reaching the people that want them. So that’s how supply affects inflation.

Now, demand-side inflation, also known as demand-pull inflation, is caused by increased demand or increased spending by people like us. We go out, we shop, and if we have extra money, we shop more, and if the economy is booming, we spend more, and these things drive prices up, too. There’s a lot of dollars chasing too few goods. So those two things have really come together over the past few years to drive inflation up.

Unlike supply-driven inflation, demand-driven inflation isn’t generally seen as transitory. In order to bring that down, you have to cool demand. You have to get people to stop spending so much. And one of the ways that we do that is by monetary policy or by the Federal Reserve increasing interest rates, which is what we’ve been seeing recently.

Liz Weston: Yes, we’ve all seen those headlines about the Federal Reserve raising interest rates to bring inflation down, but let’s talk about how that really works. What’s the connection? Why does raising interest rates help fight inflation and bring prices down?

Liz Renter: So it cools demand by making things more expensive. If interest rates are higher on loans like car loans or home loans, personal loans, higher on your credit card balance, you’re going to be less likely to spend with those things, right? Another side of that is if interest rates are higher on savings accounts, for example, you’re going to be less likely to spend and more likely to park your money. So that’s how raising interest rates helps cool demand. People are less likely to spend as much, which slows price growth and helps bring inflation in.

One of the things I want to call out is that takes time. It’s not like the Fed increases rates and demand comes down. It’s not that simple. It generally takes 12 months, sometimes more for us to begin to see the impact of those rising rates in the inflation data. As a matter of fact, we’re just now beginning to see the impact of the Fed raising rates that began a year ago. But it’s still too high. The Fed would like to see it at 2%.

So one more thing I’d like to say is it moves slowly, and the Fed is in the business of using numbers, but also fortune-telling, if they’re having to look at the most recent data available is at least a month old, and they’re looking at that and saying, “OK, what are these numbers telling us? What impact have we had already? What’s the trajectory of that? How will it change things if we lower them or raise rates even more?” So it’s a lot of guesswork and a lot of hoping they take the right steps at the right time.

Liz Weston: OK. All right, we’re going to talk now about what we can do. We know what we can’t control, which is a broader economy, but what can we control? As we mentioned before, the prices for a lot of things we need are more expensive right now, so how do we find room in our budgets? What can we be doing right now when our paycheck isn’t stretching so far? And I think, Kim, you can help with that.

Kim Palmer: I will definitely try to help with that. I think when we’re going through a big transition or something stressful like this — like these stubbornly higher prices — one really helpful place to start is just to look back at our spending. So take some time and look at how has inflation impacted your spending? Where is your money going right now? Has your grocery bill changed so much? I know mine has over the last few months. And so just tracking it can be a really good place to start.

And then from there you can apply a basic budgeting overview, something like the 50-30-20 budget, which basically means 50% of your take-home pay is going towards needs. That’s things like housing and food. 30% going towards wants, and then 20% is for any debt repayment that you have and savings. It’s not a hard-and-fast rule, but I think it can be a really helpful way of just ballparking where you want your money to be going. So that’s a really great place to start.

From there, I think it’s a great time to just take a deeper look. So where can we cut back? Where can we save? And one really helpful place to look is that recurring cost, those expenses that are coming up month after month. So things like streaming services, maybe it’s time to cut back on some of those. Maybe you’ve already done that and it’s time to get even more strategic and look really hard, for example, at how you’re spending on food or being more strategic about planning out your meals, that kind of thing.

When it comes to shopping, I think one really helpful approach, something I try to do, instead of buying something right away, when you realize you want something or even need something, see if you can just press pause either for 24 hours or even as long as a month. That just gives you more time to decide, “Do I really need this or can I skip it?” And it also gives you a chance to get the lowest price possible if you can wait for a sale.

A third approach to consider right now that I think a lot of people are looking at is just how can you increase your income? That’s the other side of the equation. Sometimes we can add a side hustle, anything that matches up with your skillset. Maybe it’s walking dogs. Maybe it’s helping people build websites. Anything entrepreneurial that you can do to just bring in more income can also help offset some of these costs.

There’s so many great websites out there — Upwork, Freelancer. If you just want a place to help you generate some ideas and think about “How can I increase my income?”, which of course would be so helpful right now.

Liz Weston: Yeah, absolutely. Now substitution is a big deal when it comes to inflation because people, when prices go up, try to look for things that are less expensive to substitute, like cheaper ingredients in your meals. What are some other ways that people can find less expensive alternatives?

Kim Palmer: Well, I think food is such an interesting category to really do a deep dive into because the fact is it’s really one of the most variable expenses in our budget. It’s so easy to start spending more on things like takeout and restaurant spending, and then that can really just spiral out of control. So just taking a pause and looking at your grocery spending. Maybe you’re already eating most of your meals at home, but you can really plan out your meals, avoid food waste, substitute some less expensive ingredients.

A really great strategy for food shopping, too, is to think about where and how you shop. A lot of grocery stores actually offer loyalty programs. So by offering your email or your phone number, you can get extra discounts when you shop. I really like the app Flipp, that’s F-L-I-P-P, just to figure out which grocery stores should I go to, because some have sales that are different from others that week. So you might even not want to go to the same store every single week. You might want to change it up based on those sales.

So just being more informed when you are shopping around to make those decisions I think can be really helpful. And I know right now it’s just thinking about the specific items, too. Things like packaged snacks I’ve noticed have gone up so much in price. So maybe instead of buying that prepackaged snack, you can actually buy the bulk size and package it out yourself. That’s a quick way to save some money.

Liz Weston: I remember my mother back in the day, back in the inflationary days, she’d take the weekly ads from the three grocery stores in our little town and she would mark the best prices on everything and she’d just do a loop, take advantage of that with coupons and the whole nine yards. Fortunately, we can get most coupons on our phones now, so it’s not quite as arduous as it might have been back in the day. But are there other things beyond food spending that people can use substitution?

Kim Palmer: There is. I think another category to take a really close look at is transportation. I know that was something that came up in the first poll that we asked people noticing prices there. So maybe it’s time, maybe you can think about carpooling more, relying on public transportation more. If you do have to buy gas, then just taking some time to shop around. An app like GasBuddy is really helpful just to make sure you’re getting the lowest price possible.

And then looking across other expenses, too, things like your cell phone service, your internet plan. Sometimes it’s really easy just to let those contracts auto-renew, but just taking a moment to instead of auto-renewing, just compare prices. See if you can switch to a lower-cost carrier. And then if you opt into automatic payments, paperless statements for a cell phone for example, you can often get additional savings. So you just have to do a little bit more work to opt into those things, but because of the recurring cost month after month, those savings really add up.

Liz Weston: And you can actually offset some of the cost of inflation with credit card rewards. If you have a cash-back card, for example, you’re getting money back. So make sure that you’ve got the best cards in your wallet and you’re not carrying debt, you’re paying it off in full every month, but using that credit card can really help as well.

Kim Palmer: That’s a good point.

Liz Weston: Thanks, Kim, so much for your insights. So now let’s talk about how inflation is affecting the debt that you have. Here’s another poll coming up shortly, has to do with the interest rates on your credit cards. And waiting, there we are. So the interest rate on your credit card cannot change after you get the card. True or false? False. 88% of you got that right. As we said earlier, rising interest rates mean that it’s more expensive to borrow money, and that can even be true of the money you’ve already borrowed. So Melissa, can you talk a little bit about that?

Melissa Lambarena: Yes. When it comes to one of the most common forms of debt, credit card debt has a high variable interest rate. So when interest rates rise, your credit card rate tends to rise as well. The good news for other types of loans, like personal loans, mortgages or car loans, is that they have a fixed interest rate, so they’re not affected when interest rates rise.

Liz Weston: That is so good to know and keep in mind. And some people might not realize that their credit card rates have been going up along with inflation. And, of course, this also applies to any new money that you need to borrow. If you’re applying for a new loan or a new credit card right now or a new mortgage, the rates are much higher typically than they were a few years ago. But what can people do about that? What should they do right now?

Melissa Lambarena: One of the most important things you can do right now is come up with a strategy to pay off that credit card debt, come up with your plan, and you can start by looking at a debt-payoff calculator. We have one on NerdWallet that you can use, and this will give you a starting point, an idea of what your monthly payments will look like and how long it can potentially take to pay it off.

And next, you want to look at what strategy you want to employ, whether it’s the avalanche method where you start paying off the high interest rate debt first or the snowball method where you start paying off the smaller debts first to gain more momentum. It’s really a matter of personal preference. There’s no right or wrong way. The point is to be taking those steps to make that progress.

And then lastly, you want to take a look at whether you can lower your interest rate through a personal loan or a 0% APR balance transfer credit card. Explore your options.

Liz Weston: That’s really great advice. And we always say if you are struggling to pay the minimums on your credit card, if you’re borrowing from one source to pay another, if you’re struggling with your debt in general, you want to talk to a legitimate credit counseling service — those are ones affiliated with the National Foundation for Credit Counseling — and a bankruptcy attorney. By talking to those two sources, you can get a very good idea of your options going forward because, unfortunately, with interest rates growing up, it’s not going to be easier to pay this debt; typically, it’s just going to get harder. So if you’re already struggling, please reach out and get some help. We have lots of resources and lots of information on the NerdWallet site.

So speaking of debt, buying a home is one of the biggest purchases and the largest amount of debt that most people will ever take on. Just because there are less than optimal economic conditions doesn’t mean that people are going to stop wanting to buy and sell houses. So let’s turn to our mortgage Nerd, Holden Lewis, for some answers.

Holden, last year was a really tough one for both home buyers and home sellers. Rates went up, and that made homes more expensive to buy. The same time prices dropped in many areas, and that discouraged sellers. So what do you expect 2023 will be like for both buyers and sellers?

Holden Lewis: OK, first, let’s just briefly talk about why 2022 was so difficult for buyers and sellers. What happened is that mortgage rates just blasted off. They were like 3 and a half percent at the beginning of 2022. They peaked at above 7% in October and November, and those rising rates, they just wrecked affordability.

So what’s the 2023 outlook? The key to the 2023 housing market is mortgage rates. If they fall to 5 and a half percent or lower, the housing market will thaw noticeably. Some economists believe mortgage rates are going to peak early this year and then they’re going to fall in the spring. Not everyone is forecasting a drop in mortgage rates to that 5 and a half percent level, but some are like the Mortgage Bankers Association. They just revised their forecast, and they believe that mortgage rates are going to hit about 5.2% toward the end of this year. And that would be good news for buyers and sellers.

I mean, home prices have fallen since last summer. A few months after mortgage rates started rising, and that’s especially evident on the West Coast and not so much on the East Coast. We might see a decline in prices in most markets, maybe edging east of the Mississippi River, but homeowners are reluctant to list their homes for sale if that means getting a higher mortgage rate on their next home. So what that means is fewer owners are going to be willing to list their properties, and that is going to restrict the supply, and that’s going to keep prices from falling a whole lot.

And finally, there’s been an increase in price reductions, and that’s just a sign that sellers are finally getting the message that they’re just not going to get the price that they could have gotten if they’d sold their house last spring.

Liz Weston: We talked about that a bit on the podcast that people were reluctant to. They knew what their house had been worth a year ago or a few months ago, and they were just unwilling to accept that they had to price it lower. But I think at the time you said something like, “The person who cuts first, cuts least.” Did I get that right?

Holden Lewis: Yeah, that’s one of the favorite sayings I’ve read. I saw it on Twitter somewhere, and I thought, “That’s perfect.”

Liz Weston: Yeah, just be realistic about the price going forward and you’ll be able to sell your house. So what if you are determined to either buy or sell a house in 2023? How should buyers and sellers approach this?

Holden Lewis: OK, let’s talk to home sellers first.

Try setting a realistic price at the beginning — one that’s going to let buyers know that you’re serious about selling. And this is going to take letting go of your ego. And really, if prices in your neighborhood are falling, and you think it’s going to take a couple of months to sell your house, then basically set the listing price near what you think it’ll be worth in two months, maybe not what it’s worth today.

If you’re buying, remember to search for homes that are priced a little bit higher than the top of your price range. For example, let’s say the maximum you’re going to be able to buy a house for is $300,000. When you’re searching online, you might look for houses up to, say, $315,000. That way, if you negotiate a 5% reduction in the price, you’ll be at your limit of $300,000.

And I mention this because boomers and Gen Xers, that’s how they sell houses. They set a price above what they think they’re going to get, and then they expect to negotiate the price down. And Gen Zers and to a lesser extent millennials, they really just want to shop for a house. They just expect people to set a more realistic price. So if you’re a Gen Zer or a millennial, you’ve got to play that boomer and Gen X game.

And then if house prices fall, it might be years before they recover. So home buyers are better off if they buy a house that they’re going to live in for more than just two or three years. So if you think that you’re going to have to move in two or three, maybe four years, maybe just keep renting. I mean, if you’re otherwise ready financially and in your life and you’re ready to settle for at least five years, then go ahead, buy that house.

Liz Weston: And that was always the classic advice about you buy a house when you’re ready to stay put for five years because typically that’s how long it takes for appreciation to offset the costs of buying and selling and moving, all that. So we’re kind of back to the classic advice. Thank you.

Holden Lewis: Exactly. We’re finally edging toward a more traditional housing market after about three years of just like, what is this?

Liz Weston: Bananas appreciation. All right, great. Thank you, Holden. Now let’s turn to our savings accounts and how inflation affects those. We recently got a text from Stephanie, and she wrote, “Hi NerdWallet. My question for you is how to protect your savings from inflation, specifically the savings you’re supposed to set aside in case of a lost job or emergency. Thanks.” So Chanelle, what would you tell Stephanie?

Chanelle Bessette: So I have some good and some bad news. As has been established, when inflation is high, it means that the value of your money has gone down. And so unfortunately, the savings account or emergency account that you have set aside with ideally three to six months’ worth of expenses, those expenses are going to cost more money when inflation is higher, which means that you need to save more in order to compensate for that.

However, the good news is that as inflation is high, the Fed starts to increase interest rates on not only loan products and things where consumers are borrowing money, but banks also respond by increasing interest rates on savings accounts and certificates of deposit.

So we’re currently seeing some really high interest rates on savings accounts, right now especially, some of the best high-yield online savings accounts that we cover are in the range of 3% or higher, sometimes even 4% or higher. So you can earn a lot more on your money right now.

Liz Weston: So it’s really worth taking a look and shopping around and seeing if you can get a better rate on your savings than you’re getting, especially at brick-and-mortar banks, right?

Chanelle Bessette: Yeah, especially at brick-and-mortar banks. They tend to be a lot lower. Some of the lowest ones are barely anything, they’ll be 0.01%. So say you have $10,000 and you’re looking to set it aside for your emergency fund; if you decide to go with one of those more traditional brick-and-mortar accounts, you’re only going to earn a dollar at the end of the year.

Whereas if you turn to an account that has 4% interest or higher, you could end up having $400 by the end of that year. So in addition to that, over the years, that really adds up with compound interest and you’ll end up having a lot more money if you put your funds into a high-yield savings account.

Liz Weston: OK, that difference can really add up over time. It may not seem like there’s a huge difference, but as you said, it can total hundreds of dollars. And just as an aside, if you have a high-yield account, make sure that you’re checking to make sure you’re getting the highest yield available. I recently had an experience with an online bank where they had shoved the legacy account holders into a very low-earning account, and it really ticked me off because I thought I was getting a great rate, and I wasn’t. So everybody take a look at what you’re actually earning. Come to NerdWallet, check some of our rates that the banks are offering and see if you can get a better deal.

All right. Well, thank you, panelists, for your great information, and now we’re turning to the Q and A section. If you haven’t already asked a question using that little Q and A button on the bottom of the screen, you can do so now. And I’m going to go through the list. Ah, Liz Renter, you’re up. OK. How does inflation factor into all the talk about a potential recession?

Liz Renter: That’s a great question because I feel like those two words are the buzzwords of the past 12 months like, “Oh, my gosh, inflation. Oh, no, a potential recession.” They’re everywhere. And as we talked about at the top of this session, not everybody really even knows necessarily what they mean.

So how does inflation factor into a recession? It’s what we’ve seen over the past few years. We’ve been in a boom. We’ve had a booming economy. Well now they’re trying to bring inflation down, and they’re trying to ease it down carefully and slowly so we don’t go into a bust because you go down dramatically too far too fast, and that’s a recession. And a recession is characterized by low inflation but also higher unemployment and an economy that isn’t as robust. It’s not as pleasant of a place to be. We would all feel that because we or people we know might be out of jobs. So that’s how it plays into it.

The Fed is in this balancing act of trying to bring inflation down but trying to bring it down at a reasonable pace and without wrecking stuff. And that’s where the term soft landing has come into play, if you’ve heard that recently. That’s what they’re hoping for. They’re hoping to bring it in with a soft landing rather than a recession.

Liz Weston: And a lot of people, when they hear recession, they think of the Great Recession, which was a huge dislocation, lots of stuff going on, really bad, lots of unemployment. It was the worst economic dislocation since the Great Depression of the ’30s. But not all recessions are like that, right? Some are much more mild.

Liz Renter: Right, exactly. And I think the consensus is that if we do enter recession on the tail end of this, it’s going to be brief, and it’s going to be mild.

Liz Weston: Great. OK, this question is for Kim. A listener mentions that you mentioned the 50-30-20 budget, but that seems impossible for me. What should you do if your essential expenses are much more than 50% of your income? Just as an aside, when I first did the 50-30-20 budget, my must-have expenses, my essentials were I think 80% or very close to 80% of my after-tax income. So, Kim, what would you recommend?

Kim Palmer: Yes, I think this brings up such an important point, which is that these budgeting ballparks that we have, these percentage allocations, it really does not necessarily apply to your situation. It’s really just some guidance that can be helpful, but especially for people that, for example, live in really high-cost areas, it can just be impossible, especially given all that we’re talking about with inflation. It can be impossible to meet those targets. So while it’s a useful target I think to have, you also have to apply it to your own situation and give yourself some flexibility.

And if you are really in a situation where you’re overwhelmed, you’re not sure how to even cover your essentials like food and housing, then it’s really time just to focus on what’s most important, which is food, housing, utilities. And you can use a really helpful resource I always like to mention, 211.org, which is a website that helps you find local resources to help you to get extra support if you’re struggling, for example, with buying food or paying bills. So that’s a great place to turn as well.

Liz Weston: Great. Thank you, Kim. All right, this question is for Chanelle. You talked about high-yield savings accounts. Do you recommend considering certificates of deposit when interest rates are so high?

Chanelle Bessette: Yeah. I know I mentioned it super briefly, but there is a pretty big distinction between savings accounts and certificates of deposit, and that’s accessibility. So CDs are designed to have your money put away for a term length, and if you try to take your money out before that term length is over, you could be hit with a penalty, meaning you’ll have to pay a fee or a percentage to get that money.

So if you have money that you’re trying to set aside for a goal that’s a little bit further down the road, CDs can be really wonderful for that because you just take a chunk of money and you’re going to earn a guaranteed rate of return. So it can be really good, say, if you’re deciding to buy a house in a year or two or you just want to maybe set aside some savings for a home renovation or something like that.

It can be really useful, so it’s definitely something to consider, but savings accounts are going to be easier to access day to day. So savings accounts are going to be better for short- to medium-term savings for things like an emergency fund.

Liz Weston: OK, great. Thank you. OK, Holden, this one is for you. The question is, is it the same with construction loans and building a home in 2023? I guess they’re referring to higher interest rates making it more costly. Can you talk a little bit about construction loans and how they might be different from a regular mortgage?

Holden Lewis: Sure. If you’re getting a construction to permanent loan, the rate on that has gone up since last year. One of the differences is that during construction, you pay only the interest on the loan, and then you pay the principal and interest after the home is ready for moving in. So that gives you a little bit of space. If you’re paying a mortgage on a house and you’re having another house built, you’re not having to pay full mortgage payments on both of them.

Now, if the interest rate is higher than you’re liking, you’re kind of stuck with it. I mean, you might have the opportunity to refinance in the next two or three years if mortgage rates fall sufficiently. And crossing fingers, I mean, I think that that will happen.

One positive development is construction times, and frankly, prices of materials. In the pandemic era, it has been taking longer to build a home than before the pandemic. And that’s because of shortages and everything from garage doors to windows to air-conditioning compressors. And those shortages had made those items more expensive, too. Those shortages are being resolved, and so construction times should shorten, and let’s hope that prices of materials go down, too.

Liz Weston: Yeah, we saw a real spike in lumber during the pandemic, and that kind of eased off, so that gives us some hope that these prices will, if not come down, at least the rate of increase will slow down.

Holden Lewis: Right.

Liz Weston: So this question is for Melissa. Are creditors, specifically credit cards, willing to lower interest rates if you call and ask them? Assuming you’re a good customer, pay on time, et cetera, is that even possible?

Melissa Lambarena: Great question. So you might have different options depending on the creditor. It might be possible to negotiate your credit card interest rate. You might have to speak to a supervisor, and if you’re able to negotiate anything, you want to get that in writing. But there might be another option as well, the question is why do you need to lower your interest rate?

Maybe you’re working on paying off debt or maybe you’re really struggling to pay off those payments, and one option that might be available — some creditors, credit card issuers offer a credit card hardship program. So you can ask about that. We saw these early in the pandemic in 2020, and they can offer a short-term way to lower your interest rates or maybe even waive some fees. It really depends on the issuer.

So that might be a potential option, but you really want to get to the core of one way you can lower your debt, and maybe that means coming up with some side income, a job on the side, or maybe lowering expenses as Kim had mentioned previously. So you really want to get to the point of that, the root of that. But it is some options that you can consider as you’re working on debt.

Liz Weston: Liz, we have another question you kind of touched on, but maybe you could expand on a little bit, which is, do we expect more inflation to come this year? And how long is this trajectory expected to last?

Liz Renter: So I think the trajectory has already changed. The direction that we’re headed is we’re coming down, meaning the rate at which prices are growing is slowing. This doesn’t mean prices are coming down. When we say inflation is coming down, that just means the growth rate is slowing. So do we expect more inflation this year? Again, I want to make sure I answer this in a way because it’s tricky wording.

So I don’t expect the inflation rate to get higher, to go back up to where it was last summer. It’s going to continue to decrease. The rate at which prices are rising is going to continue to decrease. Monetary policy is working, so it’s going to continue to come down. The Fed aims for 2% inflation, so we’ve got a ways to go before we get there. Will we see it by the end of this year? Kind of doubt it, but it’s headed in the right direction.

Liz Weston: Thank you, Liz. Here’s a question we don’t have a specific Nerd to answer. It’s how does inflation affect insurance rates? And I can take a whack at this because I was just writing about it, and inflation can definitely affect insurance because the cost of things is going up. I mean, think about what’s happened with car prices, used cars and new cars, how expensive they’ve gotten because there was a chip shortage and supply chain disruptions, and then there’s labor costs going up.

So I had a friend who had a car that would have been totaled, got into an accident, and in a normal market it would not have been worth fixing. But because used car prices were so high, she got it fixed, and she’s driving it today. So without all those costs going up, the cost of insuring that car is going to be higher, the same for your home.

And if you own a home and haven’t checked your coverage recently, highly, highly, highly recommend you do so because as we talked about, the construction costs have gone through the roof literally, and you want to make sure that you have enough money to rebuild your house if it burns down or is destroyed in a disaster.

Most homeowners in normal markets are underinsured. They don’t have enough money to rebuild their houses; they don’t have enough coverage to rebuild their houses. Right now, that problem is likely just getting more acute. So if you can put this on your to-do list, put it on your calendar to take a look at your coverage and talk to your insurer and make sure that you have enough.

Quick way to do that is to find a contractor who’s building in your area and just ask them, “OK, what’s the square footage cost of building in this neighborhood?” That can give you a ballpark to work with.

So take a look, and if you haven’t shopped around for car insurance for a while, do that. Because again, insurers are not really rewarding you for being loyal most of the time. They’re expecting you not to shop around, so they’re raising your rates. You can come on NerdWallet, we have a lot of information about shopping for insurance so that you can get the best rates.

But I think that’s all the time we have now. And I want to thank our panelists for all the great information and for participating today. This was really super interesting, at least for me, and I hope really helpful for our audience. And thank you to our audience for attending and asking such great questions.

You can find lots more information on inflation, on recessions, on everything to do with personal finance on NerdWallet’s site. And if you haven’t already, let me recommend that you create a free NerdWallet account that gives you personalized money insights.

It can help you keep tabs on your credit score, which is really important, can help you track your net worth, get first access to breaking news that affects your money. In general, it’s just a really handy app to have on your phone or on your computer.

So inflation can be really scary and disruptive to our finances, but this will not last forever. And there are some good things that will come from it. There are ways that you can help yourself, so please focus on what you can control and recognize what you can’t. Again, thanks everybody for your time.